{kind=link}

MOSCOW — For three years, the Kremlin’s “Fortress Economy” seemed to defy the laws of gravity. Buoyed by high energy prices and a swift pivot to Asian markets, Russia’s war machine appeared self-sustaining. But as the conflict officially enters its fourth year, the golden age of the Russian war economy has hit a wall of high interest rates, widening sanctions, and a burgeoning crisis in its most vital organ: the oil industry.

The Profitability Cliff

The most alarming signal for Moscow isn’t coming from the front lines, but from the oil patches of Siberia. According to recent Rosstat data, nearly half of Russia’s oil and gas companies are now operating at a loss. Between January and November 2025, these companies collectively bled 575 billion rubles ($7.5 billion).

The crisis is claiming its first victims among small-to-mid-sized producers. In the last few weeks, a wave of bankruptcies has swept the sector:

- First Oil Group: The state bank VTB has initiated bankruptcy proceedings against this producer in the Khanty-Mansiysk region over $78 million in unpaid debt.

- NC Yangpur: A subsidiary representing Belarusian interests in Yamalo-Nenets has entered insolvency.

- Astrakhan & Gorniy Oil: Both have collapsed under the weight of tax claims and falling margins.

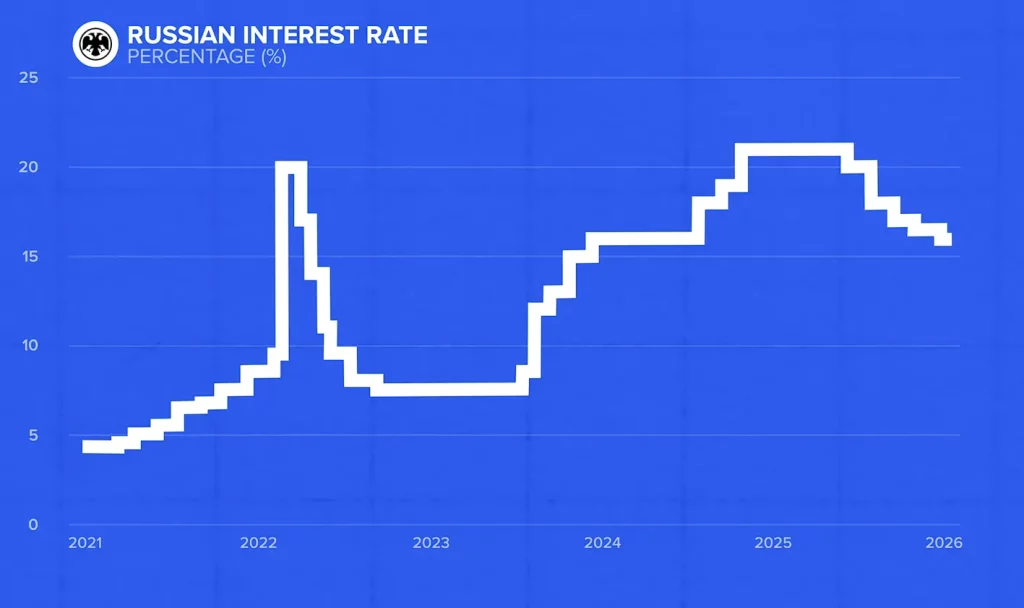

The Central Bank reports that the oil and gas sector now leads the nation in debt restructurings, with 2.7 trillion rubles in loans being rewritten as companies struggle to service debt at a punishing 16% to 21% interest rate.

The “India Pivot” Reverses

While 2023 was the year of the Russian-Indian energy romance, 2026 has brought a messy breakup. Following a trade deal with the U.S. and increased pressure on sanctioned tankers, India’s imports of Russian crude have plummeted to 1.1 million barrels per day (bpd) this January—the lowest level since late 2022.

To compensate, Moscow has been forced to “gorge” the Chinese market with heavily discounted crude. While China’s imports reached a record 2.1 million bpd this month, the cost has been steep. Russian Urals are now trading at discounts of $27 to $30 per barrel below the Brent benchmark.

“Russia and Iran are now cannibalizing each other’s market share in China,” says one energy analyst. “The Kremlin is running out of options other than slashing prices to levels that barely cover the cost of extraction.”

Draining the Rainy Day Fund

The fiscal fallout is becoming impossible to hide. Russia’s budget deficit widened to 2.6% of GDP in 2025, a dangerous figure for a nation locked out of international credit markets. To plug the hole, Finance Minister Anton Siluanov recently announced plans to tighten the “fiscal rule” to protect what remains of the National Wealth Fund (NWF).

The liquid portion of the NWF has dwindled significantly. Current estimates suggest that at today’s oil prices, the fund could be exhausted within 15 months.

| Economic Indicator | February 2023 | February 2026 |

| Key Interest Rate | 7.5% | 16% – 21% |

| Urals Crude Discount | ~$13/bbl | ~$27/bbl |

| Oil Sector Profitability | High | 50% Unprofitable |

| Annual Inflation | ~11% | ~6.3% (Target 4%) |

A Gamble on Political Will

Despite the “systemic degradation” of the economy, President Vladimir Putin shows no sign of de-escalation. The strategy has shifted from economic growth to economic survival—a gamble that the West will lose its political appetite for supporting Ukraine before Russia runs out of liquid cash.

However, with production drilling at its lowest rate since the pandemic and the “shadow fleet” facing tighter UK and US sanctions, the physical capacity to maintain this war machine is no longer a given. For the first time since the invasion began, Russia is consistently pumping below its OPEC quota, not by choice, but because the wells are simply starting to run dry.