{kind=link}

After several months of strong headline data, new economic figures released Friday suggest the U.S. economy may be losing some momentum, even as underlying conditions remain relatively solid by international standards.

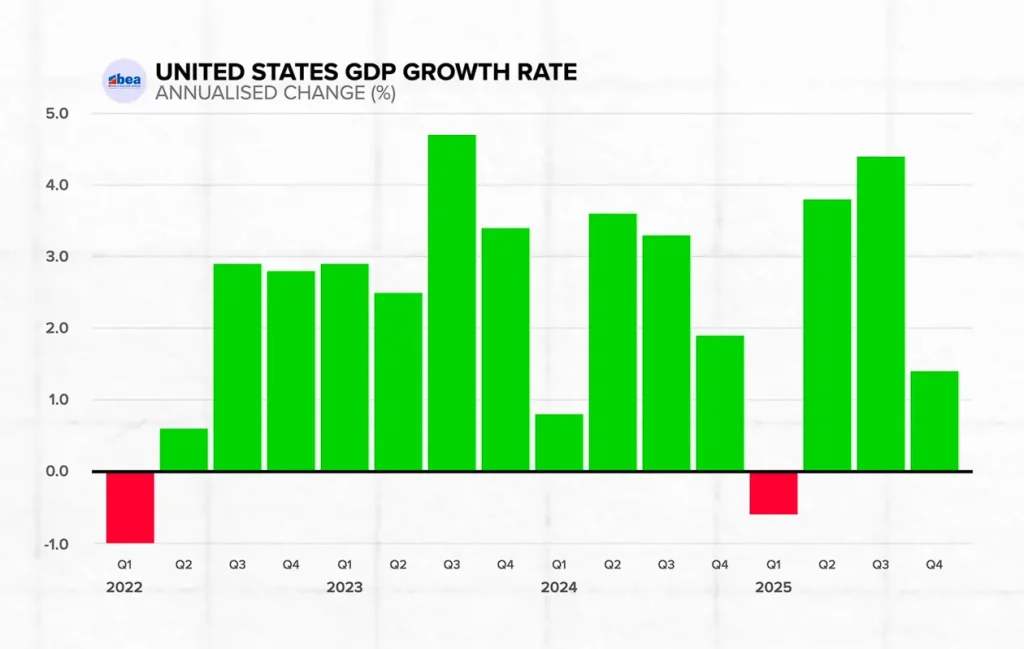

The Commerce Department reported that gross domestic product (GDP) grew at an annualized rate of 1.4% in the fourth quarter, down from 4.4% in the third quarter. The slowdown was broader than many forecasters had anticipated and was driven by declines in government spending, softer consumer activity, and a weaker contribution from net exports.

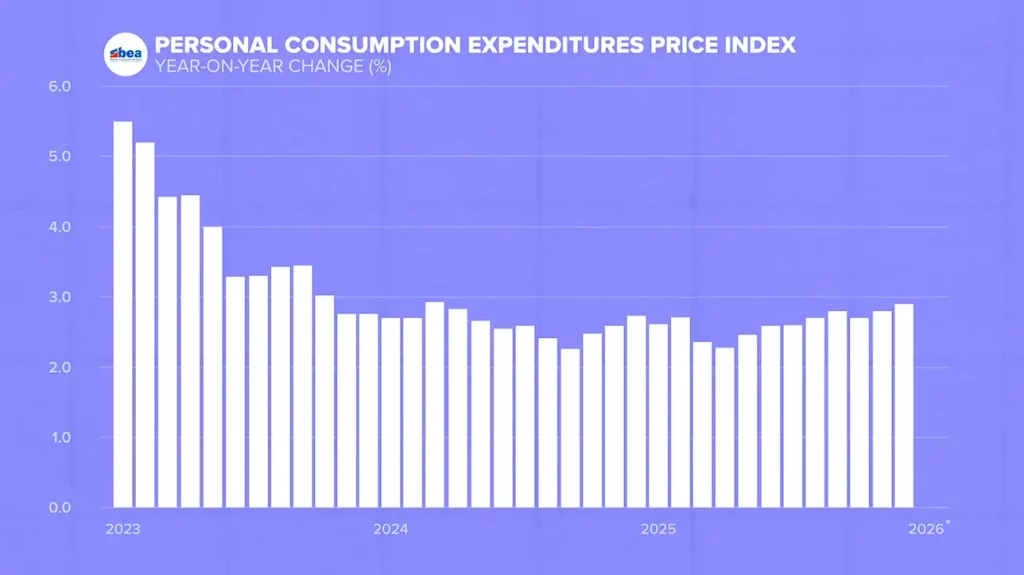

At the same time, inflation as measured by the Personal Consumption Expenditures (PCE) index — the preferred gauge of the Federal Reserve — rose to 2.9% in December, above both November’s reading and the Fed’s 2% target. The data complicates expectations for interest rate cuts in the near term.

Together, the figures have prompted renewed debate about the trajectory of the economy in 2026.

Government Spending and the Shutdown Effect

A significant portion of the fourth-quarter slowdown stemmed from reduced government spending, largely due to the 43-day federal government shutdown in October and November. Economists estimate that the shutdown subtracted roughly one percentage point from headline GDP growth.

Because government spending is expected to resume, some analysts view this drag as temporary. If so, first-quarter growth could rebound mechanically as federal outlays normalize.

Net Exports Lose Momentum

Net exports — defined as exports minus imports — were roughly flat in the fourth quarter. In the second and third quarters, a narrowing trade deficit had boosted overall GDP growth.

That earlier improvement, however, was influenced by unusually large swings in imports of pharmaceuticals and gold, as well as movements in the dollar. As those effects stabilized, the trade deficit widened again late in the year, removing a previous source of support for growth.

While many economists do not view the trade deficit itself as inherently problematic, fluctuations in net exports can have a significant short-term impact on quarterly GDP readings.

Consumer Spending Slows

Consumer spending, which accounts for roughly two-thirds of U.S. economic activity, continued to expand but at a slower pace. Consumption rose at a 1.5% annualized rate in the fourth quarter, the weakest reading since the beginning of the year and below expectations.

Some analysts suggest that earlier strength in spending may have been partly driven by households accelerating purchases amid policy uncertainty, including anticipated tariff changes and shifts in tax incentives. Inflation can also encourage consumers to bring forward purchases if they expect prices to rise further.

Recent data showing a decline in the household savings rate and weaker consumer sentiment surveys have added to concerns that spending growth could moderate further if income gains do not accelerate.

Investment Remains Strong

One area of continued strength was business investment, particularly in technology and artificial intelligence–related sectors. Tech investment rose to a record share of GDP, reflecting ongoing capital spending in data centers, semiconductor infrastructure, and related industries.

Economists note that sustained investment growth could help support productivity over the medium term, even if consumer activity cools.

Inflation Remains Above Target

The increase in the PCE inflation measure to 2.9% may prove more consequential for monetary policy. While inflation has fallen significantly from its peak, the latest reading suggests progress toward the Fed’s 2% target may be uneven.

The Federal Reserve has signaled that future interest rate decisions will depend on incoming data. A stabilization or renewed rise in inflation could lead policymakers to delay or scale back anticipated rate cuts.

Legal Uncertainty Around Tariffs

Adding to the week’s developments, the Supreme Court ruled that the majority of tariffs implemented under former President Donald Trump were unlawful. The decision introduces uncertainty around trade policy and potential fiscal implications, though the full economic effects remain unclear.

Trade policy has been a central element of recent economic strategy, and changes to tariff structures could affect government revenue, supply chains, and pricing dynamics depending on how policymakers respond.

Outlook

Despite the slowdown, several indicators remain relatively strong. Unemployment is low by historical standards, corporate balance sheets are generally stable, and underlying growth — excluding the temporary shutdown effect — appears closer to moderate expansion than contraction.

Still, the combination of softer consumer spending, flat net exports, and firmer inflation has shifted the tone of economic assessments. Whether the fourth-quarter data represents a temporary pause or the beginning of a broader cooling phase will depend on developments in consumer demand, inflation trends, fiscal policy, and global conditions in the months ahead.